Global value chains (GVCs) represent a foundational element of contemporary industrial organization and international competitiveness. For the European Union (EU), the ability to understand and strategically position itself within these networks is essential to advancing its core objectives of resilience, competitiveness, and strategic autonomy – principles now embedded in the EU’s new Competitiveness Compass.[1]

Unlike traditional trade, GVCs focus on the exchange of value-added (VA) for production purposes rather than the delivery of final goods. They outline the movement of intermediate inputs that traverse borders through a sequence of activities and tasks implemented in different economies, contributing to the creation of products that are, in effect, “made in the world.”

This newsletter presents selected empirical insights into the patterns of VA flows to and from the EU as a whole, with particular emphasis on the roles of the United States (US) and China as key trade partners and participants in EU value chains. The analysis draws on the GRinGVCs database[2], a novel dataset offering metrics and indicators that enable the mapping and monitoring of VA trade—the core dimension of GVCs—at both the sectoral level (2-digit NACE Rev.2 classification) and the country level, covering 76 global economies, including all 27 EU Member States.

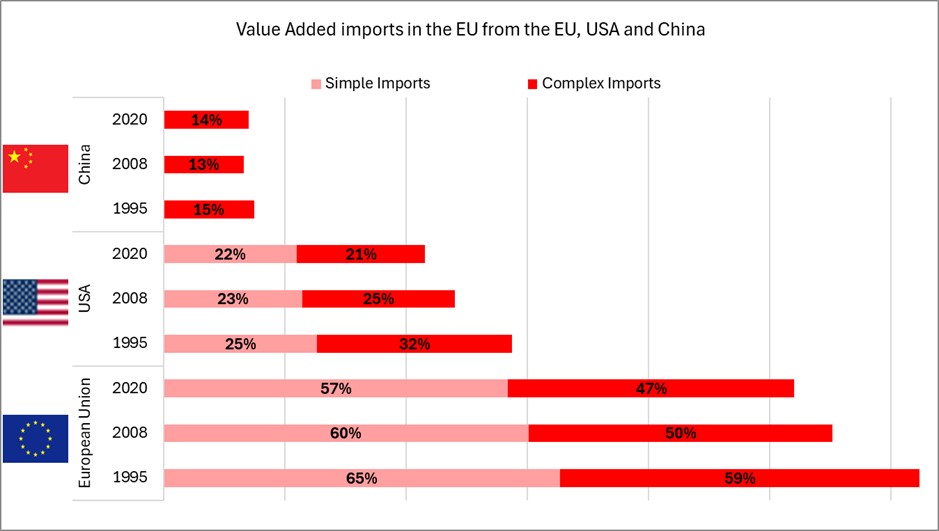

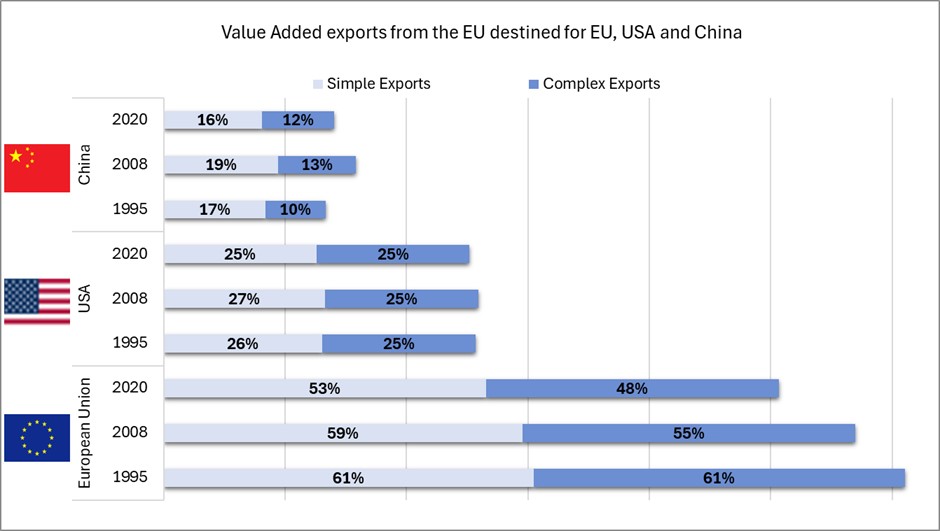

To illustrate these dynamics, we present two graphs in Figure 1, which depict EU inward (import) and outward (export) VA flows for the years 1995, 2008, and 2020. These flows are depicted as shares of the overall VA imports/exports in each year of reference, and encompass both intra-EU and extra-EU production networks—the former reflecting trade within the Single Market, and the latter capturing linkages with the US and China. The graphs distinguish between simple activities, defined as direct trade transactions where VA crosses borders for production purposes only one time, and complex activities, which involve VA crossing borders multiple times through successive production stages. [3]

(a) EU imports of VA

(b) EU imports of VA

Figure 1: Value-added (VA) imports (panel a) and exports (panel b) from and to the EU in 1995, 2008, and 2020. Trade partners include the EU (Single Market trade), the USA and China. Shares correspond to overall VA imports/exports per mode (simple and complex) of each economy over the three reference years.

Insights for the EU: Internal Integration as a Structural Asset

The EU is characterized by a high degree of internal interdependence. Intra-EU flows of VA consistently account for 50–60% of total transactions, underscoring the Single Market’s role as a deeply integrated production space. Major economies such as Germany, France, and Italy function as pivotal nodes, while smaller member states are also strongly embedded in these networks. This dense web of interconnections enhances the Union’s resilience but also raises questions about the balance between internal reliance and external diversification. The trend evolution depicted from 1995 to 2020 suggests a gradual outward orientation (i.e., lower intra-EU shares), reflecting the EU’s ambition to strengthen its global footprint while preserving the Single Market as its foundation.

Insights for the US: Diversification and Limited EU Dependence

The United States maintains a diversified portfolio of production linkages. Approximately one quarter of US value added flows involve the EU, indicating a moderate but stable level of interdependence. Stronger linkages exist with Canada and Mexico, as well as with Japan and China. A modest decline in EU-related flows in 2020 is consistent with US policy efforts to reduce external dependencies and reinforce domestic production capacity. For the EU, this underlines the importance of positioning itself as a reliable partner while recognizing the limits of its role within US-centered production networks.

Insights for China: Regional Anchoring and Productive Autonomy

China’s integration with the EU remains comparatively limited, with less than 20% of VA flows linked to the EU. Instead, China’s production system is anchored in East Asia, with significant interdependencies involving Japan, Korea, and Taiwan. At the same time, China demonstrates a strong orientation toward domestic self-sufficiency, with a substantial share of value added produced and consumed internally. This dual strategy of regional integration and productive autonomy presents both opportunities and constraints for the EU in deepening its engagement with China.

The evidence highlights the EU’s distinctive position: a highly integrated internal market that provides resilience and scale, but one that must also adapt to an evolving global environment. These messages are also transmitted through the Commission’s strategic documents, where strategic autonomy and the role of the EU has been central to the overall discussion regarding the rejuvenation of the Union’s competitiveness. To safeguard competitiveness and reduce vulnerabilities, the EU should:

- Strengthen European value chains in critical sectors such as semiconductors, clean technologies, and health industries.

- Promote cross-border industrial alliances that leverage the Single Market’s scale while fostering innovation capacity.

- Advance diversification strategies to reduce over-reliance on any single external partner.

Strategic autonomy should be understood not as isolation, but as the capacity to act independently and effectively within a multipolar global economy. In this context, the EU’s role is pivotal as a leader in strategic and emerging value chains – both in competition and in cooperation with its major global partners. The Single Market remains the cornerstone of this ambition, providing the EU with the depth of integration and the scale necessary to materialize its global competitiveness aspirations.

[1] https://commission.europa.eu/topics/eu-competitiveness/competitiveness-compass_en

[2] The GRinGVCs database is a novel dataset developed within the framework of the project “GRinGVCs: Leveraging Global Value Chains for Innovation and Competitiveness – The Case of Greece”. The project was funded under Greece’s Recovery and Resilience Facility (RRF), as part of the “Greece 2.0” programme, through the Hellenic Foundation for Research and Innovation (HFRI/ΕΛΙΔΕΚ) (Project ID: HFRI-016667). It was implemented by the Laboratory of Industrial and Energy Economics (LIEE) at the National Technical University of Athens (NTUA), which serves as the Greek institutional member of the PromethEUs network. For more information and the database, see here.

[3] For example, in the case of EU complex exports to the US, VA originated from the EU has passed through multiple stages before reaching the US economy as a final production and consumption destination. On the other hand, EU complex imports from China imply that Chinese VA reached the EU as final destination after multiple preceding production stages.